6 Sergio and Gerard each inherited a half interest in a property, ‘Hilltop’, in October 2005. ‘Hilltop’ had a probate valueof £124,000, but in November 2005 it was badly damaged by fire. In January 2006 the insurance company madea payment of £81,700 each

题目

6 Sergio and Gerard each inherited a half interest in a property, ‘Hilltop’, in October 2005. ‘Hilltop’ had a probate value

of £124,000, but in November 2005 it was badly damaged by fire. In January 2006 the insurance company made

a payment of £81,700 each to Sergio and Gerard. In February 2006 Sergio and Gerard each spent £55,500 of the

insurance proceeds on restoring the property. ‘Hilltop’ was worth £269,000 following the restoration work. In July

2006, Sergio and Gerard sold ‘Hilltop’ for £310,000.

Sergio is 69 years old and a widower with three adult children and seven grandchildren. His annual income consists

of a pension of £9,900 and interest of £300 on savings of £7,600 in a bank deposit account. Sergio owns his home

but no other significant assets. He plans to buy a domestic rental property with the proceeds from the sale of ‘Hilltop’,

such that on his death he will have a significant asset which can be sold and divided between the members of his

family.

Gerard is 34 years old. He is employed by Fizz plc on a salary of £66,500 per year together with a performance

related bonus. Gerard estimates that he will receive a bonus in December 2007 of £4,500, in line with previous

years, and that his taxable benefits in the tax year 2007/08 will amount to £7,140. He also expects to receive

dividends from UK companies of £1,935 and bank interest of £648 in the tax year 2007/08. Gerard intends to set

up a personal pension plan in August 2007. He has not made any pension contributions in the past and proposes to

use part of the proceeds from the sale of ‘Hilltop’ to make the maximum possible tax allowable contribution.

Fizz plc has announced that it intends to replace the performance related bonus scheme with a share incentive plan,

also linked to performance, with effect from 6 April 2008. Gerard estimates that Fizz plc will award him free shares

worth £2,100 each year. He will also purchase partnership shares worth £700 each year and, as a result, will be

awarded matching shares (further free shares) worth £1,400.

Required:

(a) Calculate the chargeable gains arising on the receipt of the insurance proceeds in January 2006 and the sale

of ‘Hilltop’ in July 2006. You should assume that any elections necessary to minimise the gain on the receipt

of the insurance proceeds have been submitted. (4 marks)

相似考题

更多“6 Sergio and Gerard each inherited a half interest in a property, ‘Hilltop’, in October 2005. ‘Hilltop’ had a probate valueof £124,000, but in November 2005 it was badly damaged by fire. In January 2006 the insurance company madea payment of £81,700 each ”相关问题

-

第1题:

(b) Ambush loaned $200,000 to Bromwich on 1 December 2003. The effective and stated interest rate for this

loan was 8 per cent. Interest is payable by Bromwich at the end of each year and the loan is repayable on

30 November 2007. At 30 November 2005, the directors of Ambush have heard that Bromwich is in financial

difficulties and is undergoing a financial reorganisation. The directors feel that it is likely that they will only

receive $100,000 on 30 November 2007 and no future interest payment. Interest for the year ended

30 November 2005 had been received. The financial year end of Ambush is 30 November 2005.

Required:

(i) Outline the requirements of IAS 39 as regards the impairment of financial assets. (6 marks)

正确答案:

(b) (i) IAS 39 requires an entity to assess at each balance sheet date whether there is any objective evidence that financial

assets are impaired and whether the impairment impacts on future cash flows. Objective evidence that financial assets

are impaired includes the significant financial difficulty of the issuer or obligor and whether it becomes probable that the

borrower will enter bankruptcy or other financial reorganisation.

For investments in equity instruments that are classified as available for sale, a significant and prolonged decline in the

fair value below its cost is also objective evidence of impairment.

If any objective evidence of impairment exists, the entity recognises any associated impairment loss in profit or loss.

Only losses that have been incurred from past events can be reported as impairment losses. Therefore, losses expected

from future events, no matter how likely, are not recognised. A loss is incurred only if both of the following two

conditions are met:

(i) there is objective evidence of impairment as a result of one or more events that occurred after the initial recognition

of the asset (a ‘loss event’), and

(ii) the loss event has an impact on the estimated future cash flows of the financial asset or group of financial assets

that can be reliably estimated

The impairment requirements apply to all types of financial assets. The only category of financial asset that is not subject

to testing for impairment is a financial asset held at fair value through profit or loss, since any decline in value for such

assets are recognised immediately in profit or loss.

For loans and receivables and held-to-maturity investments, impaired assets are measured at the present value of the

estimated future cash flows discounted using the original effective interest rate of the financial assets. Any difference

between the carrying amount and the new value of the impaired asset is an impairment loss.

For investments in unquoted equity instruments that cannot be reliably measured at fair value, impaired assets are

measured at the present value of the estimated future cash flows discounted using the current market rate of return for

a similar financial asset. Any difference between the previous carrying amount and the new measurement of theimpaired asset is recognised as an impairment loss in profit or loss. -

第2题:

(ii) The property of the former administrative centre of Tyre is owned by the company. Tyre had decided in the year

that the property was surplus to requirements and demolished the building on 10 June 2006. After demolition,

the company will have to carry out remedial environmental work, which is a legal requirement resulting from the

demolition. It was intended that the land would be sold after the remedial work had been carried out. However,

land prices are currently increasing in value and, therefore, the company has decided that it will not sell the land

immediately. Tyres uses the ‘cost model’ in IAS16 ‘Property, plant and equipment’ and has owned the property

for many years. (7 marks)

Required:

Advise the directors of Tyre on how to treat the above items in the financial statements for the year ended

31 May 2006.

(The mark allocation is shown against each of the above items)

正确答案:

(ii) Former administrative building

The land and buildings of the former administrative centre are accounted for as separate elements. The demolition of the

building is an indicator of the impairment of the property under IAS36. The building will not generate any future cash flows

and its recoverable amount is zero. Therefore, the carrying value of the building will be written down to zero and the loss

charged to profit or loss in the year to 31 May 2006 when the decision to demolish the building was made. The land value

will be in excess of its carrying amount as the company uses the cost model and land prices are rising. Thus no impairment

charge is recognised in respect of the land.

The demolition costs will be expensed when incurred and a provision for environmental costs recognised when an obligation

arises, i.e. in the financial year to 31 May 2007. It may be that some of these costs could be recognised as site preparation

costs and be capitalised under IAS16.

The land will not meet the criteria set out in IFRS5 ‘Non-current Assets Held for Sale and Discontinued Operations’ as a noncurrent

asset which is held for sale. IFRS5 says that a non-current asset should be classified as ‘held for sale’ if its carrying

amount will be recovered principally through a sale transaction rather than through continuing use. However, the non-current

asset must be available for immediate sale and must be actively marketed at its current fair value (amongst other criteria) and

these criteria have not been met in this case.

When the building has been demolished and the site prepared, the land could be considered to be an investment property

and accounted for under IAS40 ‘Investment Property’ where the fair value model allows gains (or losses) to be recognised inprofit or loss for the period. -

第3题:

2 Graeme, aged 57, is married to Catherine, aged 58. They work as medical consultants, and both are higher rate

taxpayers. Barry, their son, is aged 32. Graeme, Catherine and Barry are all UK resident, ordinarily resident and

domiciled. Graeme has come to you for some tax advice.

Graeme has invested in shares for some time, in particular shares in Thistle Dubh Limited. He informs you of the

following transactions in Thistle Dubh Limited shares:

(i) In December 1986, on the death of his grandmother, he inherited 10,000 £1 ordinary shares in Thistle Dubh

Limited, an unquoted UK trading company providing food supplies for sporting events. The probate value of the

shares was 360p per share.

(ii) In March 1992, he took up a rights issue, buying one share for every two held. The price paid for the rights

shares was £10 per share.

(iii) In October 1999, the company underwent a reorganisation, and the ordinary shares were split into two new

classes of ordinary share – ‘T’ shares and ‘D’ shares, each with differing rights. Graeme received two ‘T’ and three

‘D’ shares for each original Thistle Dubh Limited share held. The market values for the ‘T’ shares and the ‘D’

shares on the date of reorganisation were 135p and 405p per share respectively.

(iv) On 1 May 2005, Graeme sold 12,000 ‘T’ shares. The market values for the ‘T’ shares and the ‘D’ shares on that

day were 300p and 600p per share respectively.

(v) In October 2005, Graeme sold all of his ‘D’ shares for £85,000.

(vi) The current market value of ‘T’ shares is 384p per share. The shares remain unquoted.

Graeme and Catherine have owned a holiday cottage in a remote part of the UK for many years. In recent years, they

have used the property infrequently, as they have taken their holidays abroad and the cottage has been let out as

furnished holiday accommodation.

Graeme and Catherine are now considering selling the UK country cottage and purchasing a holiday villa abroad.

Initially they plan to let this villa out on a furnished basis, but following their anticipated retirement, would expect to

occupy the property for a significant part of the year themselves, possibly moving to live in the villa permanently.

Required:

(a) Calculate the total chargeable gains arising on Graeme’s disposals of ‘T’ and ‘D’ ordinary shares in May and

October 2005 respectively. (7 marks)

正确答案:

-

第4题:

For this part, assume today’s date is 15 August 2005.

5 (a) Donald is aged 22, single, and about to finish his university education. He has plans to start up a business selling

computer games, and intends to start trading on 1 April 2006, making up accounts to 31 March annually.

He believes that his business will generate cash (equal to taxable profits) of £47,500 in the first year. He

originally intended to operate as a sole trader, but he has recently discovered that as an alternative, he could

operate through a company. He has been advised that if this is the case, he can take a maximum gross salary

of £42,648 out of the company.

Required:

(i) Advise Donald on the income tax (IT), national insurance (NIC) and corporation tax (CT) liabilities he

will incur for the year ended 31 March 2007 trading under each of the two alternative business

structures (sole trade/company). Your advice should be supported by calculations of disposable income

for both alternatives assuming that in the company case, he draws the maximum salary stated.

(7 marks)

正确答案:

-

第5题:

6 Alasdair, aged 42, is single. He is considering investing in property, as he has heard that this represents a good

investment. In order to raise the funds to buy the property, he wants to extract cash from his personal company, Beezer

Limited, whose year end is 31 December.

Beezer Limited was formed on 1 May 1998 with £1,000 of capital issued as 1,000 £1 ordinary shares, and traded

until 1 January 2005 when Alasdair sold the trade and related assets. The company’s only asset is cash of

£120,000. Alasdair wants to extract this cash from the company with the minimum amount of tax payable. He is

considering either, paying himself a dividend of £120,000, on 31 March 2006, after which the company would have

no assets and be wound up or, leaving the cash in the company and then liquidating the company. Costs of liquidation

of £5,000 would then be incurred.

Since Beezer Limited ceased trading, Alasdair has been taken on as a partner at a marketing firm, Gallus & Co. He

estimates his profit share for the year of assessment 2005/06 will be £30,000. He has not made any capital disposals

in the current tax year.

Alasdair wishes to reinvest the cash extracted from Beezer Limited in property but is not sure whether he should invest

directly in residential or commercial property, or do so via some form. of collective investment. He is aware that Gallus

& Co are looking to rent a new warehouse which could be bought for £200,000. Alasdair thinks that he may be able

to buy the warehouse himself and lease it to his firm, but only if he can borrow the additional money to buy the

property.

Alasdair has a 25% shareholding in another company, Glaikit Limited, whose year end is 31 March. The remaining

shares in this company are held by his friend, Gill. Alasdair is considering borrowing £15,000 from Glaikit Limited

on 1 January 2006. He does not intend to pay any interest on the loan, which is likely to be written off some time

in 2007. Alasdair does not have any connection with Glaikit Limited other than his shareholding.

Required:

(a) Advise Alasdair whether or not a dividend payment will result in a higher after-tax cash sum than the

liquidation of Beezer Limited. Assume that either the dividend would be paid on 31 March 2006 or the

liquidation would take place on 31 March 2006. (9 marks)

Assume that Beezer Limited has always paid corporation tax at or above the small companies rate of 19%

and that the tax rates and allowances for 2004/05 apply throughout this part.

正确答案:

-

第6题:

2 Benny Korere has been employed as the sales director of Golden Tan plc since 1994. He earns an annual salary of

£32,000 and is provided with a petrol-driven company car which has a CO2 emission rate of 187g/km and had a

list price when new of £22,360. In August 2003, when he was first provided with the car, Benny paid the company

£6,100 towards the capital cost of the car. Golden Tan plc does not pay for any of Benny’s private petrol and he is

also required to pay his employer £18 per month as a condition of being able to use the car for private purposes.

On 1 December 2006 Golden Tan plc notified Benny that he would be made redundant on 28 February 2007. On

that day the company will pay him his final month’s salary together with a payment of £8,000 in lieu of the three

remaining months of his six-month notice period in accordance with his employment contract. In addition the

company will pay him £17,500 in return for agreeing not to work for any of its competitors for the six-month period

ending 31 August 2007.

On receiving notification of his redundancy, Benny immediately contacted Joe Egmont, the managing director of

Summer Glow plc, who offered him a senior management position leading the company’s expansion into Eastern

Europe. Summer Glow plc is one of Golden Tan plc’s competitors and one of the most innovative companies in the

industry, although not all of its strategies have been successful.

Benny has agreed to join Summer Glow plc on 1 September 2007 for an annual salary of £39,000. On the day he

joins the company, Summer Glow plc will grant him an option to purchase 10,000 ordinary shares in the company

for £2·20 per share under an unapproved share option scheme. Benny can exercise the option once he has been

employed for six months but must hold the shares for at least a year before he sells them.

The new job will require Benny to spend a considerable amount of time in London. Summer Glow plc has offered

Benny the exclusive use of a flat that the company purchased on 1 June 2003 for £165,000; the flat is currently

rented out. The flat will be made available from 1 September 2007. The company will pay all of the utility bills

relating to the flat as well as furnishing and maintaining it. Summer Glow plc has also suggested that if Benny would

rather live in a more central part of the city, the company could sell the existing flat and buy a more centrally located

one, of the same value, with the proceeds.

On 15 March 2007 Benny intends to sell 5,800 shares in Mahana plc, a quoted company, for £24,608. His

transactions in the company’s shares have been as follows:

£

June 1988 Purchased 8,400 shares 6,744

February 1996 Sale of rights nil paid 610

January 2005 Purchased 1,300 shares 2,281

The sale of rights, nil paid, was not treated as a part disposal of Benny’s holding in Mahana plc.

Benny’s shareholding in Mahana plc represents less than 1% of the company’s issued ordinary share capital. He will

not make any other capital disposals in 2006/07.

In addition to his employment income, Benny receives rental income of £4,000 (net of deductible expenses) each

year. He normally submits his tax return in August but he has not yet prepared his return for 2005/06. He expects

to be very busy in December and January and is planning to prepare his tax return in late February 2007.

Required:

(a) Calculate Benny’s employment income for 2006/07. (4 marks)

正确答案:

-

第7题:

4 (a) For this part, assume today’s date is 1 March 2006.

Bill and Ben each own 50% of the ordinary share capital in Flower Limited, an unquoted UK trading company

that makes electronic toys. Flower Limited was incorporated on 1 August 2005 with 1,000 £1 ordinary shares,

and commenced trading on the same day. The business has been successful, and the company has accumulated

a large cash balance of £180,000, which is to be used to purchase a new factory. However, Bill and Ben have

received an offer from a rival company, which they are considering. The offer provides Bill and Ben with two

alternative methods of payment for the purchase of their shares:

(i) £480,000 for the company, inclusive of the £180,000 cash balance.

(ii) £300,000 for the company assuming the cash available for the factory purchase is extracted prior to sale.

Bill and Ben each currently receive a gross salary of £3,750 per month from Flower Limited. Part of the offer

terms is that Bill and Ben would be retained as employees of the company on the same salary.

Neither Bill nor Ben has used any of their capital gains tax annual exemption for the tax year 2005/06.

Required:

(i) Calculate which of the following means of extracting the £180,000 from Flower Limited on 31 March

2006 will result in the highest after tax cash amount for Bill and Ben:

(1) payment of a dividend, or

(2) payment of a salary bonus.

You are not required to consider the corporation tax (CT) implications for Flower Limited in your

answer. (5 marks)

正确答案:

As a result, Bill and Ben would each be better off by £15,005 (69,142 – 54,137). If the cash were extracted by way

of dividend.

Tutorial note: In this answer the employers’ national insurance liability on the salary has been ignored. Credit would be

given to a candidate who recognised this issue. -

第8题:

1 Alvaro Pelorus is 47 years old and married to Maria. The couple have two children, Vito and Sophie, aged 22 and

19 years respectively. Alvaro and Maria have lived in the country of Koruba since 1982. On 1 July 2005 the family

moved to the UK to be near Alvaro’s father, Ray, who was very ill. Alvaro and Maria are UK resident, but not ordinarily

resident in the tax years 2005/06 and 2006/07. They are both domiciled in the country of Koruba.

On 1 February 2007 Ray Pelorus died. He was UK domiciled, having lived in the UK for the whole of his life. For the

purposes of inheritance tax, his death estate consisted of UK assets, valued at £870,000 after deduction of all

available reliefs, and a house in the country of Pacifica valued at £94,000. The executors of Ray’s estate have paid

Pacifican inheritance tax of £1,800 and legal fees of £7,700 in respect of the sale of the Pacifican house. Ray left

the whole of his estate to Alvaro.

Ray had made two gifts during his lifetime:

(i) 1 May 2003: He gave Alvaro 95 acres of farm land situated in the UK. The market value of the land was

£245,000, although its agricultural value was only £120,000. Ray had acquired the land on

1 January 1996 and granted an agricultural tenancy on that date. Alvaro continues to own the

land as at today’s date and it is still subject to the agricultural tenancy.

(ii) 1 August 2005: He gave Alvaro 6,000 shares valued at £183,000 in Pinger Ltd, a UK resident trading

company. Gift relief was claimed in respect of this gift. Ray had acquired 14,000 shares in

Pinger Ltd on 1 April 1997 for £54,600.

You may assume that Alvaro is a higher rate taxpayer for the tax years 2005/06 and 2006/07. In 2006/07 he made

the following disposals of assets:

(i) On 1 July 2006 he sold the 6,000 shares in Pinger Ltd for £228,000.

(ii) On 1 September 2006 he sold 2,350 shares in Lapis Inc, a company resident in Koruba, for £8,270. Alvaro

had purchased 5,500 shares in the company on 1 September 2002 for £25,950.

(iii) On 1 December 2006 he transferred shares with a market value of £74,000 in Quad plc, a UK quoted company,

to a UK resident discretionary trust for the benefit of Vito and Sophie. Alvaro had purchased these shares on

1 January 2006 for £59,500.

Alvaro has not made any other transfers of value for the purposes of UK inheritance tax. He owns the family house

in the UK as well as shares in UK and Koruban companies and commercial rental property in the country of Koruba.

Maria has not made any transfers of value for the purposes of UK inheritance tax. Her only significant asset is the

family home in the country of Koruba.

Alvaro and his family expect to return to their home in the country of Koruba in October 2007 once Ray’s affairs have

been settled. There is no double taxation agreement between the UK and Koruba.

Required:

(a) Calculate the inheritance tax (IHT) payable as a result of the death of Ray Pelorus. Explain the availability

or otherwise of agricultural property relief and business property relief on the two lifetime gifts made by Ray.

(8 marks)

正确答案:

-

第9题:

(b) The directors of Carver Ltd are aware that some of the company’s shareholders want to realise the value in their

shares immediately. Accordingly, instead of investing in the office building or the share portfolio they are

considering two alternative strategies whereby, following the sale of the company’s business, a payment will be

made to the company’s shareholders.

(i) Liquidate the company. The payment by the liquidator would be £126 per share.

(ii) The payment of a dividend of £125 per share following which a liquidator will be appointed. The payment

by the liquidator to the shareholders would then be £1 per share.

The company originally issued 20,000 £1 ordinary shares at par value to 19 members of the Cutler family.

Following a number of gifts and inheritances there are now 41 shareholders, all of whom are family members.

The directors have asked you to attend a meeting to set out the tax implications of these two alternative strategies

for each of the two main groups of shareholders: adults with shareholdings of more than 500 shares and children

with shareholdings of 200 shares or less.

Required:

Prepare notes explaining:

– the amount chargeable to tax; and

– the rates of tax that will apply

in respect of each of the two strategies for each of the two groups of shareholders ready for your meeting

with the directors of Carver Ltd. You should assume that none of the shareholders will have any capital

losses either in the tax year 2007/08 or brought forward as at 5 April 2007. (10 marks)

Note:

You should assume that the rates and allowances for the tax year 2006/07 will continue to apply for the

foreseeable future.

正确答案:

-

第10题:

(c) In October 2004, Volcan commenced the development of a site in a valley of ‘outstanding natural beauty’ on

which to build a retail ‘megastore’ and warehouse in late 2005. Local government planning permission for the

development, which was received in April 2005, requires that three 100-year-old trees within the valley be

preserved and the surrounding valley be restored in 2006. Additions to property, plant and equipment during

the year include $4·4 million for the estimated cost of site restoration. This estimate includes a provision of

$0·4 million for the relocation of the 100-year-old trees.

In March 2005 the trees were chopped down to make way for a car park. A fine of $20,000 per tree was paid

to the local government in May 2005. (7 marks)

Required:

For each of the above issues:

(i) comment on the matters that you should consider; and

(ii) state the audit evidence that you should expect to find,

in undertaking your review of the audit working papers and financial statements of Volcan for the year ended

31 March 2005.

NOTE: The mark allocation is shown against each of the three issues.

正确答案:

(c) Site restoration

(i) Matters

■ The provision for site restoration represents nearly 2·5% of total assets and is therefore material if it is not

warranted.

■ The estimated cost of restoring the site is a cost directly attributable to the initial measurement of the tangible fixed

asset to the extent that it is recognised as a provision under IAS 37 ‘Provisions, Contingent Liabilities and

Contingent Assets’ (IAS 16 ‘Property, Plant and Equipment’).

■ A provision should not be recognised for site restoration unless it meets the definition of a liability, i.e:

– a present obligation;

– arising from past events;

– the settlement of which is expected to result in an outflow of resources embodying economic benefits.

■ The provision is overstated by nearly $0·34m since Volcan is not obliged to relocate the trees and de facto has

only an obligation of $60,000 as at 31 March 2005 (being the penalty for having felled them). When considered

in isolation, this overstatement is immaterial (representing only 0·2% of total assets and 3·6% of PBT).

■ It seems that even if there are local government regulations calling for site restoration there is no obligation unless

the penalties for non-compliance are prohibitive (unlike the fines for the trees).

■ It is unlikely that commencement of site development has given rise to a constructive obligation, since past actions

(disregarding the preservation of the trees) must dispel any expectation that Volcan will honour any pledge to

restore the valley.

■ Whether commencing development of the site, and destroying the trees, conflicts with any statement of socioenvironmental

responsibility in the annual report.

(ii) Audit evidence

■ A copy of the planning application and permission granted setting out the penalties for non-compliance.

■ Payment of $60,000 to local government in May 2005 agreed to the bank statement.

■ The present value calculation of the future cash expenditure making up the $4·0m provision.

Tutorial note: Evidence supporting the calculation of $0·4m is irrelevant as there is no liability to be provided for.

■ Agreement that the pre-tax discount rate used reflects current market assessments of the time value of money (as

for (a)).

■ Asset inspection at the site as at 31 March 2005.

■ Any contracts entered into which might confirm or dispute management’s intentions to restore the site. For

example, whether plant hire (bulldozers, etc) covers only the period over which the warehouse will be constructed

– or whether it extends to the period in which the valley would be ‘made good’. -

第11题:

2 Assume that today’s date is 1 July 2005.

Jan is aged 45 and single. He is of Danish domicile but has been working in the United Kingdom since 1 May 2004

and intends to remain in the UK for the medium to long term. Although Jan worked briefly in the UK in 1986, he

has forgotten how UK taxation works and needs some assistance before preparing his UK income tax return.

Jan’s salary from 1 May 2004 was £74,760 per annum. Jan also has a company car – a Jaguar XJ8 with a list price

of £42,550 including extras, and CO2 emissions of 242g/km. The car was available to him from 1 July 2004. Free

petrol is provided by the company. Jan has other taxable benefits amounting to £3,965.

Jan’s other 2004/05 income comprises:

£

Dividend income from UK companies (cash received) 3,240

Interest received on an ISA account 230

Interest received on a UK bank account 740

Interest remitted from an offshore account (net of 15% withholding tax) 5,100

Income remitted from a villa in Portugal (net of 45% withholding tax) 4,598

The total interest arising on the offshore account was £9,000 (gross). In addition, Jan has not remitted other

Portuguese rental income arising in the year, totalling a further £1,500 (gross).

Jan informs you that his employer is thinking of providing him with rented accommodation while he looks for a house

to buy. The accommodation would be a two bedroom flat, valued at £155,000 with an annual value of £6,000. It

would be made available from 6 August 2005. The company will pay the rent of £600 per month for the first six

months. All other bills will be paid by Jan.

Jan also informs you that he has 25,000 ordinary shares in Gilet Ltd (‘Gilet’), an unquoted UK trading company. He

has held these shares since August 1986 when he bought 2,500 shares at £4.07 per share. In January 1994, a

bonus issue gave each shareholder nine shares for each ordinary share held. In the last week all Gilet’s shareholders

have received an offer from Jumper plc (‘Jumper’) who wishes to acquire the shares. Jumper has offered the following:

– 3 shares in Jumper (currently trading at £3.55 per share) for every 5 shares in Gilet, and

– 25p cash per share

Required:

(a) Calculate Jan’s 2004/05 income tax (IT) payable. (11 marks)

正确答案:

-

第12题:

问答题The cost of hiring a private rail carriage is shared equally by all the passengers who paid an exact number of pounds which was less than £100 each. The carriage has seats for 50 passengers and the total bill amounts to £1887. How many seats were not occupied?正确答案: 13seats (37 people each paid £51.)解析:

(根据题目要求可知,1887英镑被一些人平分,人数少于50,每人所付钱数少于100英镑,可知如果分解1887的话,符合条件的两个因子应一个小于50,一个小于100。因为1887=3×17×37,即1887=3×629,或者1887=37×51,可知是37位乘客,每位乘客交了51英镑,则空座为13个。) -

第13题:

(b) Misson has purchased goods from a foreign supplier for 8 million euros on 31 July 2006. At 31 October 2006,

the trade payable was still outstanding and the goods were still held by Misson. Similarly Misson has sold goods

to a foreign customer for 4 million euros on 31 July 2006 and it received payment for the goods in euros on

31 October 2006. Additionally Misson had purchased an investment property on 1 November 2005 for

28 million euros. At 31 October 2006, the investment property had a fair value of 24 million euros. The company

uses the fair value model in accounting for investment properties.

Misson would like advice on how to treat these transactions in the financial statements for the year ended 31

October 2006. (7 marks)

Required:

Discuss the accounting treatment of the above transactions in accordance with the advice required by the

directors.

(Candidates should show detailed workings as well as a discussion of the accounting treatment used.)

正确答案:

(b) Inventory, Goods sold and Investment property

The inventory and trade payable initially would be recorded at 8 million euros ÷ 1·6, i.e. $5 million. At the year end, the

amount payable is still outstanding and is retranslated at 1 dollar = 1·3 euros, i.e. $6·2 million. An exchange loss of

$(6·2 – 5) million, i.e. $1·2 million would be reported in profit or loss. The inventory would be recorded at $5 million at the

year end unless it is impaired in value.

The sale of goods would be recorded at 4 million euros ÷ 1·6, i.e. $2·5 million as a sale and as a trade receivable. Payment

is received on 31 October 2006 in euros and the actual value of euros received will be 4 million euros ÷ 1·3,

i.e. $3·1 million.

Thus a gain on exchange of $0·6 million will be reported in profit or loss.

The investment property should be recognised on 1 November 2005 at 28 million euros ÷ 1·4, i.e. $20 million. At

31 October 2006, the property should be recognised at 24 million euros ÷ 1·3, i.e. $18·5 million. The decrease in fair value

should be recognised in profit and loss as a loss on investment property. The property is a non-monetary asset and any foreign

currency element is not recognised separately. When a gain or loss on a non-monetary item is recognised in profit or loss,

any exchange component of that gain or loss is also recognised in profit or loss. If any gain or loss is recognised in equity ona non-monetary asset, any exchange gain is also recognised in equity. -

第14题:

2 The draft financial statements of Rampion, a limited liability company, for the year ended 31 December 2005

included the following figures:

$

Profit 684,000

Closing inventory 116,800

Trade receivables 248,000

Allowance for receivables 10,000

No adjustments have yet been made for the following matters:

(1) The company’s inventory count was carried out on 3 January 2006 leading to the figure shown above. Sales

between the close of business on 31 December 2005 and the inventory count totalled $36,000. There were no

deliveries from suppliers in that period. The company fixes selling prices to produce a 40% gross profit on sales.

The $36,000 sales were included in the sales records in January 2006.

(2) $10,000 of goods supplied on sale or return terms in December 2005 have been included as sales and

receivables. They had cost $6,000. On 10 January 2006 the customer returned the goods in good condition.

(3) Goods included in inventory at cost $18,000 were sold in January 2006 for $13,500. Selling expenses were

$500.

(4) $8,000 of trade receivables are to be written off.

(5) The allowance for receivables is to be adjusted to the equivalent of 5% of the trade receivables after allowing for

the above matters, based on past experience.

Required:

(a) Prepare a statement showing the effect of the adjustments on the company’s net profit for the year ended

31 December 2005. (5 marks)

正确答案:

-

第15题:

4 Assume today’s date is 5 February 2006.

Joanne is 37, she was born and until 2005 had lived all her life in Germany. She recently married Fraser, aged 38,

who is a UK resident, but who worked briefly in Germany. They have no children.

The couple moved to the UK to live permanently on 9 October 2005. Joanne was employed by an American company

in Germany, and she continued to work for them in the UK until the end of November 2005. Her earnings from the

American company were £5,000 per month. Joanne has not remitted any of the income she earned in Germany prior

to her arrival in the UK.

Joanne resigned from her job at the end of November 2005. The company did not hold her to the three months notice

stipulated in her contract, but still paid her for that period. In total, Joanne paid £4,200 in UK income tax under PAYE

for the tax tear 2005/06.

Joanne also wishes to sell the shares she holds in a German listed company. The shareholding cost the equivalent of

£3,500 in September 1986, and its current value is £21,500. She intends to sell the shares in March 2006 and to

invest the proceeds from the sale in the UK. Joanne has made no other capital disposals in the year.

Prior to her leaving employment, Joanne investigated the possibility of starting her own business providing a German

translation service for UK companies, and took some advice on the matter. She paid consultancy fees of £5,000

(excluding value added tax (VAT)) and bought a computer for £2,000 (excluding VAT), both on 23 October 2005.

Joanne started trading on 1 December 2005. She made sales of £2,000 in December, and estimates that her sales

will rise by £1,000 every month to a maximum of £7,000 per month. Joanne believes that her monthly expenses of

£400 (excluding VAT) will remain constant. Her year end will be 31 March, and the first accounts will be drawn up

to 31 March 2006.

Although Joanne has registered her business for tax purposes with the Revenue, she has not registered for VAT and

is unsure what is required of her in this respect.

Required:

(a) State, giving reasons, whether Joanne will be treated as resident or non-resident in the UK for the year of

assessment 2005/06, together with the basis on which her income and gains of that year will be subject to

UK taxation. (3 marks)

正确答案:

(a) Joanne will be treated as UK resident from the day she arrives in the UK, as she has stated her intention to move permanently

to the UK. Her income from this point will be taxable in the UK, although she will receive a full personal allowance

(unapportioned) for the year. Income earned in the UK will be taxable, but income earned abroad in Germany will not be

taxed unless it is remitted to the UK.

Although Joanne is UK resident, she is not UK domiciled. Thus, while capital gains on UK assets will be taxable, gains on

assets held overseas are taxable only to the extent that the proceeds of the sale are remitted to the UK. As Joanne intends to

remit the proceeds from selling her shares in Germany, the gain will be taxable in the UK. -

第16题:

(b) Donald actually decided to operate as a sole trader. The first year’s results of his business were not as he had

hoped, and he made a trading loss of £8,000 in the year to 31 March 2007. However, trading is now improving,

and Donald has sufficient orders to ensure that the business will make profits of at least £30,000 in the year to

31 March 2008.

In order to raise funds to support his business over the last 15 months, Donald has sold a painting which was

given to him on the death of his grandmother in January 1998. The probate value of the painting was £3,200,

and Donald sold it for £8,084 (after deduction of 6% commission costs) in November 2006.

He also sold other assets in the year of assessment 2006/07, realising further chargeable gains of £8,775 (after

indexation of £249 and taper relief of £975).

Required:

(i) Calculate the chargeable gain on the disposal of the painting in November 2006. (4 marks)

正确答案:

-

第17题:

3 Assume that today’s date is 10 May 2005.

You have recently been approached by Fred Flop. Fred is the managing director and 100% shareholder of Flop

Limited, a UK trading company with one wholly owned subsidiary. Both companies have a 31 March year-end.

Fred informs you that he is experiencing problems in dealing with aspects of his company tax returns. The company

accountant has been unable to keep up to date with matters, and Fred also believes that mistakes have been made

in the past. Fred needs assistance and tells you the following:

Year ended 31 March 2003

The corporation tax return for this period was not submitted until 2 November 2004, and corporation tax of £123,500

was paid at the same time. Profits chargeable to corporation tax were stated as £704,300.

A formal notice (CT203) requiring the company to file a self-assessment corporation tax return (dated 1 February

2004) had been received by the company on 4 February 2004.

A detailed examination of the accounts and tax computation has revealed the following.

– Computer equipment totalling £50,000 had been expensed in the accounts. No adjustment has been made in

the tax computation.

– A provision of £10,000 was made for repairs, but there is no evidence of supporting information.

– Legal and professional fees totalling £46,500 were allowed in full without any explanation. Fred has

subsequently produced the following analysis:

Analysis of legal & professional fees

£

Legal fees on a failed attempt to secure a trading loan 15,000

Debt collection agency fees 12,800

Obtaining planning consent for building extension 15,700

Accountant’s fees for preparing accounts 14,000

Legal fees relating to a trade dispute 19,000

– No enquiry has yet been raised by the Inland Revenue.

– Flop Ltd was a large company in terms of the Companies Act definition for the year in question.

– Flop Ltd had taxable profits of £595,000 in the previous year.

Year ended 31 March 2004

The corporation tax return has not yet been submitted for this year. The accounts are late and nearing completion,

with only one change still to be made. A notice requiring the company to file a self-assessment corporation tax return

(CT203) dated 27 July 2004 was received on 1 August 2004. No corporation tax has yet been paid.

1 – The computation currently shows profits chargeable to corporation tax of £815,000 before accounting

adjustments, and any adjustments for prior years.

– A company owing Flop Ltd £50,000 (excluding VAT) has gone into liquidation, and it is unlikely that any of this

money will be paid. The money has been outstanding since 3 September 2003, and the bad debt will need to

be included in the accounts.

1 Fred also believes there are problems in relation to the company’s VAT administration. The VAT return for the quarter

ended 31 March 2005 was submitted on 5 May 2005, and VAT of £24,000 was paid at the same time. The previous

return to 31 December 2004 was also submitted late. In addition, no account has been made for the VAT on the bad

debt. The VAT return for 30 June 2005 may also be late. Fred estimates the VAT liability for that quarter to be £8,250.

Required:

(a) (i) Calculate the revised corporation tax (CT) payable for the accounting periods ending 31 March 2003

and 2004 respectively. Your answer should include an explanation of the adjustments made as a result

of the information which has now come to light. (7 marks)

(ii) State, giving reasons, the due payment date of the corporation tax (CT) and the filing date of the

corporation tax return for each period, and identify any interest and penalties which may have arisen to

date. (8 marks)

正确答案:(a) Calculation of corporation tax

Year ended 31 March 2003

Corporation tax payable

There are three adjusting items:.

(i) The computers are capital items, as they have an enduring benefit. These need to be added back in the Schedule D

Case I calculation, and capital allowances claimed instead. The company is not small or medium by Companies Act

definitions and therefore no first year allowances are available. Allowances of £12,500 (50,000 x 25%) can be claimed,

leaving a TWDV of £37,500.

(ii) The provision appears to be general in nature. In addition there is insufficient information to justify the provision and it

should be disallowed until such times as it is released or utilised.

(iii) Costs relating to trading loan relationships are allowable, as are costs relating to the trade (debt collection, trade disputes

and accounting work). Costs relating to capital items (£5,700) are not allowable so will have to be added back.

Total profit chargeable to corporation tax is therefore £704,300 + 50,000 – 12,500 + 10,000 + 5,700 = 757,500. There are two associates, and therefore the 30% tax rate starts at £1,500,000/2 = £750,000. Corporation tax payable is 30% x£757,500 = £227,250.

Payment date

Although the rate of tax is 30% and the company ‘large’, quarterly payments will not apply, as the company was not large in the previous year. The due date for payment of tax is therefore nine months and one day after the end of the tax accounting period (31 March 2003) i.e. 1 January 2004.

Filing date

This is the later of:

– 12 months after the end of the period of account: 31 March 2004

– 3 months after the date of the notice requiring the return 1 May 2004

i.e. 1 May 2004.

-

第18题:

3 On 1 January 2007 Dovedale Ltd, a company with no subsidiaries, intends to purchase 65% of the ordinary share

capital of Hira Ltd from Belgrove Ltd. Belgrove Ltd currently owns 100% of the share capital of Hira Ltd and has no

other subsidiaries. All three companies have their head offices in the UK and are UK resident.

Hira Ltd had trading losses brought forward, as at 1 April 2006, of £18,600 and no income or gains against which

to offset losses in the year ended 31 March 2006. In the year ending 31 March 2007 the company expects to make

further tax adjusted trading losses of £55,000 before deduction of capital allowances, and to have no other income

or gains. The tax written down value of Hira Ltd’s plant and machinery as at 31 March 2006 was £96,000 and

there will be no fixed asset additions or disposals in the year ending 31 March 2007. In the year ending 31 March

2008 a small tax adjusted trading loss is anticipated. Hira Ltd will surrender the maximum possible trading losses

to Belgrove Ltd and Dovedale Ltd.

The tax adjusted trading profit of Dovedale Ltd for the year ending 31 March 2007 is expected to be £875,000 and

to continue at this level in the future. The profits chargeable to corporation tax of Belgrove Ltd are expected to be

£38,000 for the year ending 31 March 2007 and to increase in the future.

On 1 February 2007 Dovedale Ltd will sell a small office building to Hira Ltd for its market value of £234,000.

Dovedale Ltd purchased the building in March 2005 for £210,000. In October 2004 Dovedale Ltd sold a factory

for £277,450 making a capital gain of £84,217. A claim was made to roll over the gain on the sale of the factory

against the acquisition cost of the office building.

On 1 April 2007 Dovedale Ltd intends to acquire the whole of the ordinary share capital of Atapo Inc, an unquoted

company resident in the country of Morovia. Atapo Inc sells components to Dovedale Ltd as well as to other

companies in Morovia and around the world.

It is estimated that Atapo Inc will make a profit before tax of £160,000 in the year ending 31 March 2008 and will

pay a dividend to Dovedale Ltd of £105,000. It can be assumed that Atapo Inc’s taxable profits are equal to its profit

before tax. The rate of corporation tax in Morovia is 9%. There is a withholding tax of 3% on dividends paid to

non-Morovian resident shareholders. There is no double tax agreement between the UK and Morovia.

Required:

(a) Advise Belgrove Ltd of any capital gains that may arise as a result of the sale of the shares in Hira Ltd. You

are not required to calculate any capital gains in this part of the question. (4 marks)

正确答案:

(a) Capital gains that may arise on the sale by Belgrove Ltd of shares in Hira Ltd

Belgrove Ltd will realise a capital gain on the sale of the shares unless the substantial shareholding exemption applies. The

exemption will be given automatically provided all of the following conditions are satisfied.

– Belgrove Ltd has owned at least 10% of Hira Ltd for a minimum of 12 months during the two years prior to the sale.

– Belgrove Ltd is a trading company or a member of a trading group during that 12-month period and immediately after

the sale.

– Hira Ltd is a trading company or the holding company of a trading group during that 12-month period and immediately

after the sale.

Hira Ltd will no longer be in a capital gains group with Belgrove Ltd after the sale. Accordingly, a capital gain, known as a

degrouping charge, may arise in Hira Ltd. A degrouping charge will arise if, at the time it leaves the Belgrove Ltd group, Hira

Ltd owns any capital assets which were transferred to it at no gain, no loss within the previous six years by a member of the

Belgrove Ltd capital gains group. -

第19题:

6 Andrew is aged 38 and is single. He is employed as a consultant by Bestadvice & Co and pays income tax at the

higher rate.

Andrew is considering investing in a new business, and to provide funds for this investment he has recently disposed

of the following assets:

(1) A short leasehold interest in a residential property. Andrew originally paid £50,000 for a 47 year lease of the

property in May 1995, and assigned the lease in May 2006 for £90,000.

(2) His holding of £10,000 7% Government Stock, on which interest is payable half-yearly on 20 April and

20 October. Andrew originally purchased this holding on 1 June 1999 for £9,980 and he sold it for £11,250

on 14 March 2005.

Andrew intends to subscribe for ordinary shares in a new company, Scalar Limited, which will be a UK based

manufacturing company. Three investors (including Andrew) have been identified, but a fourth investor may also be

invited to subscribe for shares. The investors are all unconnected, and would subscribe for shares in equal measure.

The intention is to raise £450,000 in this manner. The company will also raise a further £50,000 from the investors

in the form. of loans. Andrew has been told that he can take advantage of some tax reliefs on his investment in Scalar

Limited, but does not know anything about the details of these reliefs

Andrew’s employer, Bestadvice & Co, is proposing to change the staff pension scheme from a defined benefit scheme

to which the firm and the employees each contribute 6% of their annual salary, to a defined contribution scheme, to

which the employees will continue to contribute 6%, but the firm will contribute 8% of their annual salary. The

majority of Andrew’s colleagues are opposed to this move, but, given the increase in the firm’s contribution rate

Andrew himself is less sure that the proposal is without merit.

Required:

(a) (i) Calculate the chargeable gain arising on the assignment of the residential property lease in May 2006.

(2 marks)

正确答案:

-

第20题:

2 Clifford and Amanda, currently aged 54 and 45 respectively, were married on 1 February 1998. Clifford is a higher

rate taxpayer who has realised taxable capital gains in 2007/08 in excess of his capital gains tax annual exemption.

Clifford moved into Amanda’s house in London on the day they were married. Clifford’s own house in Oxford, where

he had lived since acquiring it for £129,400 on 1 August 1996, has been empty since that date although he and

Amanda have used it when visiting friends. Clifford has been offered £284,950 for the Oxford house and has decided

that it is time to sell it. The house has a large garden such that Clifford is also considering an offer for the house and

a part only of the garden. He would then sell the remainder of the garden at a later date as a building plot. His total

sales proceeds will be higher if he sells the property in this way.

Amanda received the following income from quoted investments in 2006/07:

£

Dividends in respect of quoted trading company shares 1,395

Dividends paid by a Real Estate Investment Trust out of tax exempt property income 485

On 1 May 2006, Amanda was granted a 22 year lease of a commercial investment property. She paid the landlord

a premium of £6,900 and also pays rent of £2,100 per month. On 1 June 2006 Amanda granted a nine year

sub-lease of the property. She received a premium of £14,700 and receives rent of £2,100 per month.

On 1 September 2006 Amanda gave quoted shares with a value of £2,200 to a registered charity. She paid broker’s

fees of £115 in respect of the gift.

Amanda began working for Shearer plc, a quoted company, on 1 June 2006 having had a two year break from her

career. She earns an annual salary of £38,600 and was paid a bonus of £5,750 in August 2006 for agreeing to

come and work for the company. On 1 August 2006 Amanda was provided with a fully expensed company car,

including the provision of private petrol, which had a list price when new of £23,400 and a CO2 emissions rate of

187 grams per kilometre. Amanda is required to pay Shearer plc £22 per month in respect of the private use of the

car. In June and July 2006 Amanda used her own car whilst on company business. She drove 720 business miles

during this two month period and was paid 34 pence per mile. Amanda had PAYE of £6,785 deducted from her gross

salary in the tax year 2006/07.

After working for Shearer plc for a full year, Amanda becomes entitled to the following additional benefits:

– The opportunity to purchase a large number of shares in Shearer plc on 1 July 2007 for £3·30 per share. It is

anticipated that the share price on that day will be at least £7·50 per share. The company will make an interestfree

loan to Amanda equal to the cost of the shares to be repaid in two years.

– Exclusive free use of the company sailing boat for one week in August 2007. The sailing boat was purchased by

Shearer plc in January 2005 for use by its senior employees and costs the company £1,400 a week in respect

of its crew and other running expenses.

Required:

(a) (i) Calculate Clifford’s capital gains tax liability for the tax year 2007/08 on the assumption that the Oxford

house together with its entire garden is sold on 31 July 2007 for £284,950. Comment on the relevance

to your calculations of the size of the garden; (5 marks)

正确答案:

-

第21题:

5 Crusoe has contacted you following the death of his father, Noland. Crusoe has inherited the whole of his father’s

estate and is seeking advice on his father’s capital gains tax position and the payment of inheritance tax following his

death.

The following information has been extracted from client files and from telephone conversations with Crusoe.

Noland – personal information:

– Divorcee whose only other relatives are his sister, Avril, and two grandchildren.

– Died suddenly on 1 October 2007 without having made a will.

– Under the laws of intestacy, the whole of his estate passes to Crusoe.

Noland – income tax and capital gains tax:

– Has been a basic rate taxpayer since the tax year 2000/01.

– Sales of quoted shares resulted in:

– Chargeable gains of £7,100 and allowable losses of £17,800 in the tax year 2007/08.

– Chargeable gains of approximately £14,000 each tax year from 2000/01 to 2006/07.

– None of the shares were held for long enough to qualify for taper relief.

Noland – gifts made during lifetime:

– On 1 December 1999 Noland gave his house to Crusoe.

– Crusoe has allowed Noland to continue living in the house and has charged him rent of £120 per month

since 1 December 1999. The market rent for the house would be £740 per month.

– The house was worth £240,000 at the time of the gift and £310,000 on 1 October 2007.

– On 1 November 2004 Noland transferred quoted shares worth £232,000 to a discretionary trust for the benefit

of his grandchildren.

Noland – probate values of assets held at death: £

– Portfolio of quoted shares 370,000

Shares in Kurb Ltd 38,400

Chattels and cash 22,300

Domestic liabilities including income tax payable (1,900)

– It should be assumed that these values will not change for the foreseeable future.

Kurb Ltd:

– Unquoted trading company

– Noland purchased the shares on 1 December 2005.

Crusoe:

– Long-standing personal tax client of your firm.

– Married with two young children.

– Successful investment banker with very high net worth.

– Intends to gift the portfolio of quoted shares inherited from Noland to his aunt, Avril, who has very little personal

wealth.

Required:

(a) Prepare explanatory notes together with relevant supporting calculations in order to quantify the tax relief

potentially available in respect of Noland’s capital losses realised in 2007/08. (4 marks)

正确答案:

-

第22题:

1 Stuart is a self-employed business consultant aged 58. He is married to Rebecca, aged 55. They have one child,

Sam, who is aged 24 and single.

In November 2005 Stuart sold a house in Plymouth for £422,100. Stuart had inherited the house on the death of

his mother on 1 May 1994 when it had a probate value of £185,000. The subsequent pattern of occupation was as

follows:

1 May 1994 to 28 February 1995 occupied by Stuart and Rebecca as main residence

1 March 1995 to 31 December 1998 unoccupied

1 January 1999 to 31 March 2001 let out (unfurnished)

1 April 2001 to 30 November 2001 occupied by Stuart and Rebecca

1 December 2001 to 30 November 2005 used occasionally as second home

Both Stuart and Rebecca had lived in London from March 1995 onwards. On 1 March 2001 Stuart and Rebecca

bought a house in London in their joint names. On 1 January 2002 they elected for their London house to be their

principal private residence with effect from that date, up until that point the Plymouth property had been their principal

private residence.

No other capital disposals were made by Stuart in the tax year 2005/06. He has £29,500 of capital losses brought

forward from previous years.

Stuart intends to invest the gross sale proceeds from the sale of the Plymouth house, and is considering two

investment options, both of which he believes will provide equal risk and returns. These are as follows:

(1) acquiring shares in Omikron plc; or

(2) acquiring further shares in Omega plc.

Notes:

1. Omikron plc is a listed UK trading company, with 50,250,000 shares in issue. Its shares currently trade at 42p

per share.

2. Stuart and Rebecca helped start up the company, which was then Omega Ltd. The company was formed on

1 June 1990, when they each bought 24,000 shares for £1 per share. The company became listed on 1 May

1997. On this date their holding was subdivided, with each of them receiving 100 shares in Omega plc for each

share held in Omega Ltd. The issued share capital of Omega plc is currently 10,000,000 shares. The share price

is quoted at 208p – 216p with marked bargains at 207p, 211p, and 215p.

Stuart and Rebecca’s assets (following the sale of the Plymouth house but before any investment of the proceeds) are

as follows:

Assets Stuart Rebecca

£ £

Family house in London 450,000 450,000

Cash from property sale 422,100 –

Cash deposits 165,000 165,000

Portfolio of quoted investments – 250,000

Shares in Omega plc see above see above

Life insurance policy note 1 note 1

Note:

1. The life insurance policy will pay out a sum of £200,000 on the death of the first spouse to die.

Stuart has recently been diagnosed with a serious illness. He is expected to live for another two or three years only.

He is concerned about the possible inheritance tax that will arise on his death. Both he and Rebecca have wills whose

terms transfer all assets to the surviving spouse. Rebecca is in good health.

Neither Stuart nor Rebecca has made any previous chargeable lifetime transfers for the purposes of inheritance tax.

Required:

(a) Calculate the taxable capital gain on the sale of the Plymouth house in November 2005 (9 marks)

正确答案:

Note that the last 36 months count as deemed occupation, as the house was Stuart’s principal private residence (PPR)

at some point during his period of ownership.

The first 36 months of the period from 1 March 1995 to 31 March 2001 qualifies as a deemed occupation period as

Stuart and Rebecca returned to occupy the property on 1 April 2001. The remainder of the period will be treated as a

period of absence, although letting relief is available for part of the period (see below).

The exempt element of the gain is the proportion during which the property was occupied, real or deemed. This is

£138,665 (90/139 x £214,160).

(2) The chargeable gain is restricted for the period that the property was let out. This is restricted to the lowest of the

following:

(i) the gain attributable to the letting period (27/139 x 214,160) = £41,599

(ii) £40,000

(iii) the total exempt PPR gain = £138,665

i.e. £40,000.

(3) The taper relief is effectively wasted, having restricted losses b/f to preserve the annual exemption. -

第23题:

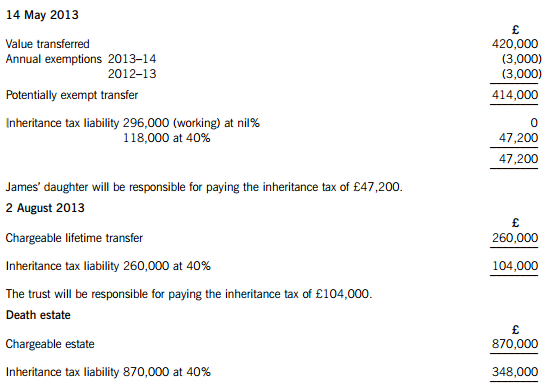

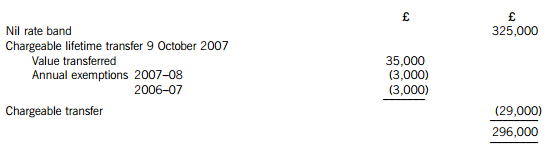

James died on 22 January 2015. He had made the following gifts during his lifetime:

(1) On 9 October 2007, a cash gift of £35,000 to a trust. No lifetime inheritance tax was payable in respect of this gift.

(2) On 14 May 2013, a cash gift of £420,000 to his daughter.

(3) On 2 August 2013, a gift of a property valued at £260,000 to a trust. No lifetime inheritance tax was payable in respect of this gift because it was covered by the nil rate band. By the time of James’ death on 22 January 2015, the property had increased in value to £310,000.

On 22 January 2015, James’ estate was valued at £870,000. Under the terms of his will, James left his entire estate to his children.

The nil rate band of James’ wife was fully utilised when she died ten years ago.

The nil rate band for the tax year 2007–08 is £300,000, and for the tax year 2013–14 it is £325,000.

Required:

(a) Calculate the inheritance tax which will be payable as a result of James’ death, and state who will be responsible for paying the tax. (6 marks)

(b) Explain why it might have been beneficial for inheritance tax purposes if James had left a portion of his estate to his grandchildren rather than to his children. (2 marks)

(c) Explain why it might be advantageous for inheritance tax purposes for a person to make lifetime gifts even when such gifts are made within seven years of death.

Notes:

1. Your answer should include a calculation of James’ inheritance tax saving from making the gift of property to the trust on 2 August 2013 rather than retaining the property until his death.

2. You are not expected to consider lifetime exemptions in this part of the question. (2 marks)

正确答案:(a) James – Inheritance tax arising on death

Lifetime transfers within seven years of death

The personal representatives of James’ estate will be responsible for paying the inheritance tax of £348,000.

Working – Available nil rate band

(b) Skipping a generation avoids a further charge to inheritance tax when the children die. Gifts will then only be taxed once before being inherited by the grandchildren, rather than twice.

(c) (1) Even if the donor does not survive for seven years, taper relief will reduce the amount of IHT payable after three years.

(2) The value of potentially exempt transfers and chargeable lifetime transfers are fixed at the time they are made.

(3) James therefore saved inheritance tax of £20,000 ((310,000 – 260,000) at 40%) by making the lifetime gift of property.